Financial abuse is the illegal or improper use of a person’s money, property, or assets, often involving coercion, deception, or exploitation. It can include actions such as misusing bank cards, pressuring someone into signing financial documents, taking possessions, abusing power of attorney, or scams that build relationships to exploit an older person’s savings or assets.

It often happens in relationships built on trust, which can make it harder to recognise, particularly when the person involved is a family member, friend, or carer.

As part of planning for and during retirement, it’s good to understand what financial abuse is and think about ways you can safeguard against financial abuse. Here’s helpful information to help you make positive choices.

Understanding financial elder abuse

Financial abuse can include misusing bank cards, forcing house mortgage deposits, taking possessions, or taking over financial authority. A loan or a guarantor signature can be “given” under duress or coercion, such as: “Just sign here Dad: If we don’t get back to the bank today, we will lose our house…”

It is illegal or improper use of money, property or other assets. For example:

- unauthorised taking of money or possessions

- misuse of power of attorney

- failure to repay loans

- use of home and/or utilities without contributing to costs

- scams that rely on establishing a relationship with the older person with the intention of exploiting their savings and/or assets, e.g. romance scams.

The impact of financial abuse

Financial elder abuse can seriously affect an older person’s independence, security, and wellbeing. It often happens in relationships built on trust and can be difficult to recognise, particularly when the person involved is a family member, friend, or carer.

Here are some things to consider:

For many older people, the impact of financial abuse can be especially severe. Recovering from a financial setback often takes much longer in later life, particularly for those on a fixed or limited income such as superannuation or savings. There may be fewer opportunities to rebuild savings, increase income, or absorb unexpected losses, which can affect housing, health, independence, and quality of life.

Age Concern supports older people to protect what matters to them by strengthening financial safety, restoring choice and control, and providing timely, compassionate support.

Request for gifts or loans can escalate family tension, particularly where:

- There are expectations around inheritance

- One family member benefits more than others

- Past financial conflict already exists, e.g., previous gifts or loans have not be repaid

- Requests become increasingly manipulative e.g., withholding of support or visits unless the loan is given

In some cases, conflict can turn into emotional or financial pressure, controlling behaviour, or exploitation. It’s important to be transparent with all family members, where possible.

Taking time to understand all options can help ensure decisions support people’s wellbeing, independence, and peace of mind.

Ways to keep your money safe

Looking after your finances is an important way to prevent financial abuse. Even small, everyday steps can make a big difference.

Tips to protection your money:

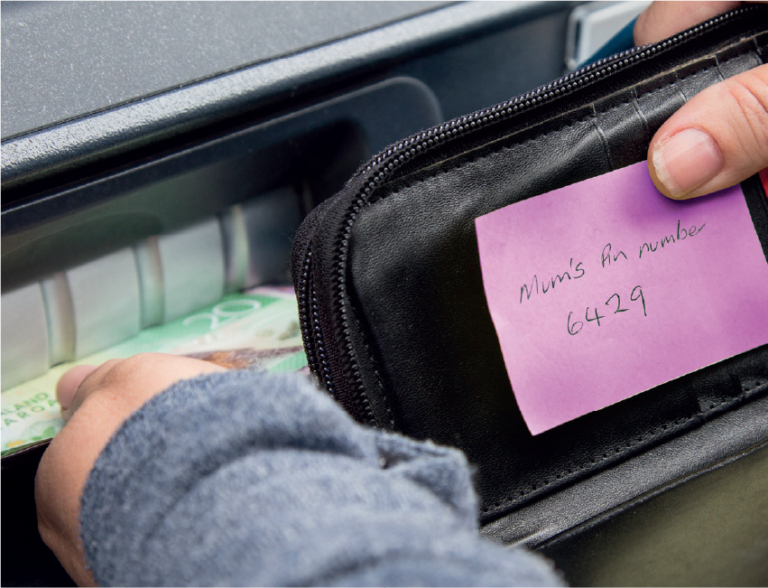

- Never share passwords, PINs, passkeys, or one‑time codes, even with family members or trusted people. Banks will never ask for these details.

- Be cautious of requests to “help manage” online banking or to set up access “just in case.”

- If someone already has access and it no longer feels right, support is available to review or change arrangements.

- Do not give your bank card or PIN to anyone, even temporarily.

- If your card has been lost, taken, or used without permission, contact your bank as soon as possible.

- Pressure to hand over a card, cash, or access to accounts can be a warning sign of financial abuse.

- Adding someone to a bank account or giving authority can reduce your control over your money.

- It’s important for you to understand what access you are giving and whether it can be changed or ended later. The banks have a Code of Practice to adhere by, so you need to allow for time when you are making changes to your bank account. This is to help safeguard your money.

- Independent advice can help ensure arrangements reflect your unique wishes and means you’re aware of the impact of your financial decisions in the short term and long term.

- Scammers may pretend to be from banks, government agencies, online retailers, or even pose as friends or romantic partners.

- Requests for urgent payments, secrecy, or personal information are common warning signs.

- Loneliness and isolation can increase vulnerability, talking with different trusted people before acting can help prevent harm.

It’s common to want to help family or loved ones. But financial decisions should always feel comfortable and fully your choice.

Older people can feel pressured, often by family members or trusted people, to take on debt that mainly benefits someone else. This may include a loan, reverse mortgage, or contributing to large purchases.

Here are some examples of elder financial abuse:

Pressure or coercion to take out the loan

One of the most common risks is pressure from others, usually family members or trusted people, to take on debt that primarily benefits the person asking for the loan. This may be pressure to take out a loan or reverse mortgage, loan a deposit for a mortgage of another house, give money towards another asset, like a car.

Warning signs include:

• Feeling rushed or told “this is the only option”

• Being encouraged to borrow so others can access money

• Being told they are “selfish” or a “burden” if they don’t agree

• Decisions being made about them rather than with them

• Suggestions to make it a verbal agreement or saying legal advice isn’t necessary

Any financial decision should be made freely and at a person’s own pace, without guilt, fear, or obligation.

Control over how the money is used

While the loan is in an older person’s name, others may try to influence or control how the money is spent, for example:

• Expecting them to hand over funds

• “Managing” the money on their behalf without transparency

• Using the money for purposes they did not agree to

This can be a form of financial abuse, even if the loan itself was legitimate.

Lack of independent advice

Not receiving independent legal and financial advice increases the risk of exploitation.

Financial elder abuse risks rise when:

• Advice is provided by someone who benefits from the loan

• The person does not fully understand interest, fees, or long‑term impacts

• Documents are signed without explanation or time to review

• English, legal terms, or financial language create barriers to understanding

Independent advice helps ensure the decision reflects the older person’s wishes and best interests, not someone else’s.

Misunderstanding long-term financial impact

A reverse mortgage, for example, can significantly reduce the value of a person’s home over time due to compounding interest. Financial abuse can occur if:

• The long term impact on their housing security is downplayed

• They are not told how the loan balance grows

• The effect on their estate or future choices is minimised

• They are encouraged to borrow more than they need

An informed decision includes understanding how long the older person plans to stay in their home and what future flexibility they may need.

Loss of future choice and independence

If a loan or reverse mortgage reduces a person’s equity significantly, it may:

• Limit options to move, downsize, or enter care later

• Reduce funds available for health or support needs

• Increase dependence on others, raising the risk of further abuse

Financial decisions that reduce independence can unintentionally increase vulnerability.

It is common for older people to be asked to be a credit contract guarantor for a family member, usually a child or grandchild. There are significant implications that it’s important to understand. Here is some helpful information to consider before becoming a guarantor or borrower for someone else.

What would being a guarantor mean?

When a person signs a form

What are the impacts of a home loan

Home loans connected to an existing property can have serious long‑term implications. In some cases, this may mean that any proceeds from the future sale of your own property could be required to pay off the guaranteed or investment loan.

Example: Tim and Trish were mortgage-free, so when their daughter, Jo asked for help to buy her first home, they took out a loan against the value of their property. Five years later, Tim and Trish decided to downsize to a smaller house, as they wanted some extra money to live during retirement. They were excited to find a new home and managed to sell their family home at the price they wanted, however, the terms of Jo’s loan meant that extra money they got from the property sale, didn’t go into their bank account – it went to pay off Jo’s property loan. This left Tim and Trish without savings, and they were unable to pay for the things they wanted to do in their retirement unless Jo repaid them the loan, which she was unable to do.

Before agreeing, it is important to ask the other person’s bank or an independent mortgage adviser to clearly explain the long‑term risks and consequences.

What to consider before being a guarantor on utility accounts

Older people are sometimes asked to act as a guarantor for telephone or electricity accounts, or to have a service connection set up in their name for another family member.

While this may seem like a simple way to help, it creates a legal responsibility – if the other person does not pay their bills, you become liable for the full amount. This can quickly lead to unexpected debt, financial stress, and even damage to credit, particularly if you are on a fixed income and unable to cover the costs. It’s important to carefully consider the risks and seek advice before agreeing to these arrangements.

The reality of acting as guarantor

The reality of acting as a guarantor includes:

- If a person acts as guarantor for a phone, power, or other service connection, they can be required to pay any large bills or overdue accounts that the other person cannot or does not pay.

- If a person acts as guarantor for a bank loan, the amount guaranteed is often unlimited and may include future borrowings, such as additional interest or overdraft increases.

- If the borrower defaults, the lender can demand repayment directly from the guarantor and does not have to exhaust other recovery options first.

- The guarantor may also be responsible for debt recovery and legal costs, not just the original amount borrowed.

- Anything offered as security can be taken and sold to repay the debt. This may include savings, investments, or even the guarantor’s home if it has been used as security.

Home loans connected to an existing property can carry significant long‑term consequences. In some cases, this may mean that any proceeds from the future sale of the guarantor’s own home must be used to repay the guaranteed loan. It is important people ask their own bank or an independent mortgage adviser to clearly explain what this could mean for you in the long term.

Feeling pressured, rushed, or told “it’s just a formality” are warning signs. It is always okay to say no, and wise to take time, and to seek independent advice before agreeing to be a guarantor.

Risks to consider with a reverse mortgage

A reverse mortgage is a type of loan that allows people, usually older homeowners, to borrow money against the value of their home. While it may provide access to cash, using a reverse mortgage to give money to someone else carries significant risks, as the loan plus interest must still be repaid, usually when the house is sold, the person moves into care, or passes away.

If the money is given to family or others who cannot repay it, the homeowner may be left with increasing debt, reduced equity in their home, and less financial security for future needs. This can affect their ability to cover living or care costs later on and may reduce what is left for their estate, so it is important to fully understand the consequences and seek independent advice before proceeding.

Acting when things go wrong

As soon as an unwise financial decision is recognised, it’s important to get legal advice immediately as there may be legal remedies available.

The lender must also keep guarantors and borrowers informed about problems with the mortgage/loan/hire purchase repayments, so it’s vital act quickly before matters come to a head.

Prevention starts with respect and choice

Financial safety is strongest when older people:

- Are respected as decision‑makers

- Have clear, reliable information

- Feel supported rather than pressured

- Stay socially connected

Financial elder abuse is never okay, but it is preventable with awareness, early support, and community care.

Several community organisations hold information sessions throughout the year. Some of the topics covered by Age Concerns are:

- Enduring power of attorney

- Wills

- Digital literacy

- Scams and fraud prevention

The best way to find out what is coming up in your community is to sign up for newsletters or follow your local Age Concern on social media.